Vital Statistics:

|

Last |

Change |

| S&P Futures |

2179.0 |

-3.0 |

| Eurostoxx Index |

340.7 |

-0.1 |

| Oil (WTI) |

47.8 |

-1.0 |

| US dollar index |

85.7 |

0.2 |

| 10 Year Govt Bond Yield |

1.56% |

|

| Current Coupon Fannie Mae TBA |

103.3 |

|

| Current Coupon Ginnie Mae TBA |

104.2 |

|

| 30 Year Fixed Rate Mortgage |

3.5 |

|

Stocks are slightly lower this morning after Stanley Fischer said the US economy was close to hitting all of the Fed's targets. Bonds and MBS are down small.

Not a lot of market-moving data this week, aside form the second revision to GDP on Friday. Note central bankers will be out in Jackson Hole this week, so there is the possibility of comments moving the markets. Otherwise, it looks to be a dull week in late August.

The Chicago Fed National Activity Index came in better than expected at .27, but the 3 month moving average is negative, indicating the economy is growing slightly below trend.

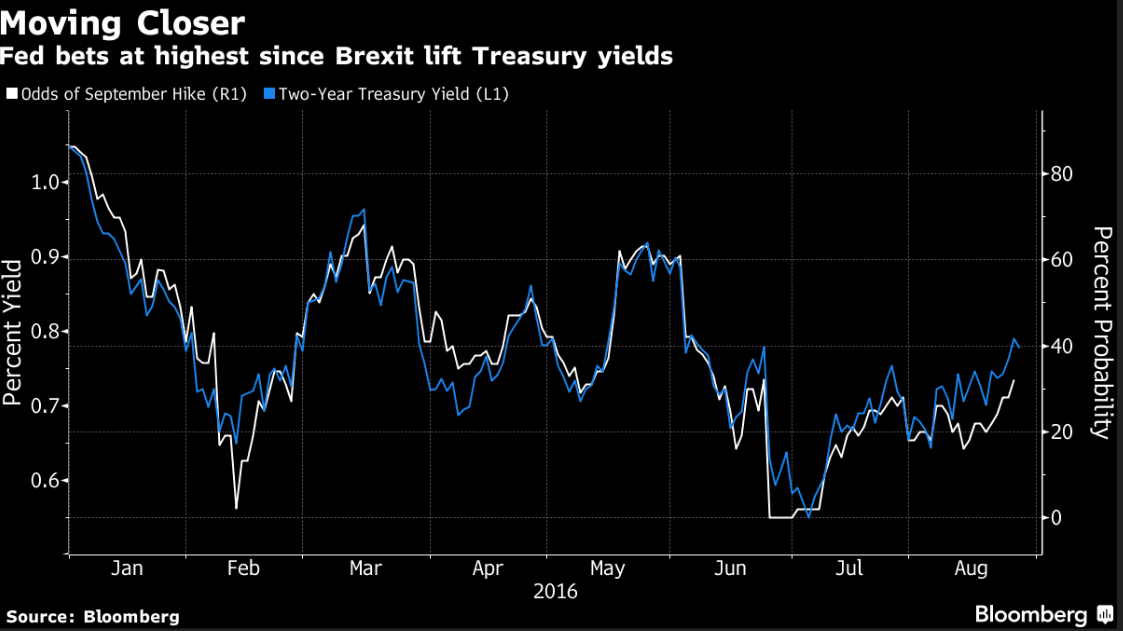

Fannie Mae is forecasting the Fed will maintain rates throughout 2016, and they believe the economy will strengthen. “Second quarter growth was a disappointment, but consumer spending appears solid heading into Q3, and we expect inventory investment to balance out after a surprising drawdown in Q2,” said Fannie Mae Chief Economist Doug Duncan. “Credit expansion, combined with improving labor market conditions and strengthening household balance sheets, should continue to support consumers, who will likely be the primary driver of growth again in the second half of the year. The positive July jobs report may encourage some Federal Open Market Committee members to argue for a Fed rate hike at the September meeting.

However, we remain convinced that the Fed will hold the target rate steady this year given global uncertainties and anemic output growth. Although much of the financial volatility from Brexit has subsided,

long-term Treasury yields continue to face downward pressure and we expect them to remain low for some time.”

More from Fannie on the housing market: “Housing market fundamentals remain a mixed bag. During the second quarter of 2016, both new and existing home sales rose to expansion highs, while single-family starts pulled back, remaining historically low for an expansion,” said Duncan. “Tight housing inventory from a lack of new construction continues to create affordability challenges, particularly at the lower end of the market. Robust rental demand during the second quarter of the year has created the lowest rental vacancy rate in decades. In addition, the homeownership rate dropped to below 63 percent in the second quarter, but we are seeing some tentative signs of

older Millennials moving toward homeownership. We expect homebuyers will benefit from improving job and wage growth, more favorable lending standards, and continued low mortgage rates through the rest of the year,

with the 30-year fixed-rate mortgage rate projected to average 3.4 percent during the fourth quarter.”

Talk about bad timing: Donald Trump got into the mortgage business in 2006. He did make an interesting point about bubbles and the madness of crowds. “Are you the type of person who takes advantage of positive situations when they present themselves, riding them out as long as they last? Or do you heed every message of doom and gloom, avoiding risks that could be some remarkable opportunities?” If you sold stocks in 1996 when Alan Greenspan discussed "irrational exuberance" in the stock market, you missed out on the lion's share of the growth. Also, the most money is made right at the end of the move when it goes parabolic.