| Last | Change | Percent | |

| S&P Futures | 1514.3 | -2.2 | -0.15% |

| Eurostoxx Index | 2616.9 | 0.2 | 0.01% |

| Oil (WTI) | 90.76 | 0.1 | 0.09% |

| LIBOR | 0.283 | -0.001 | -0.35% |

| US Dollar Index (DXY) | 82.31 | -0.004 | 0.00% |

| 10 Year Govt Bond Yield | 1.84% | 0.00% | |

| RPX Composite Real Estate Index | 194.9 | 0.2 |

Markets are slightly lower this morning after China imposed new measures to slow its housing bubble. There isn't much in the way of economic data this week with the exception of the jobs report, which was moved to this week. Bonds and MBS are flat.

While the unemployment rate stays stubbornly in the high 7s, there are signs under the surface that things are getting better. The median duration of joblessness fell to 16 weeks in January from 25 weeks in June 2010. American aged 45-55 experienced the biggest turnaround, and this would address one of the biggest achilles heels to the economy: that many people in their prime earnings years are on the bench, which crimps spending. Nobel Laureate Dale Mortensen views this as evidence that the US labor market will not enter hysteresis, or permanently higher joblessness, which happened in Europe in the 80s.

Is slower economic growth the "new normal?" There are a few explanations why the economic recovery has been so slow. The first is simply bad luck. A series of exogenous events (the Euro crisis, crises in Washington, the Japanese tsunami) keep delivering blows to the economy just as it is getting going. The second is the view of Kevin Warsh, which holds that bad policy decisions in the aftermath of the financial crisis - overregulation and a focus on short-term stimulus measures) have left the economy weakened. The last is the view of the Keynsians, who argue that the stimulus was not enough, we need to do more, and as long as the bond market is willing to lend to us at sub 2% rates, we should borrow as much as we need to upgrade our infrastructure and hire millions of unemployed workers in the process.

FWIW, I believe that all of these explanations have a kernel of truth, but miss the big picture - that we are recovering from an asset bubble, and the de-leveraging that follows takes a long time to work through. When people borrow en masse to fund asset purchases, the debt remains even if the asset falls in value. That debt has to be dealt with, and someone has to eat the losses. While Washington would love to figure out a way to short-circuit this process, there isn't a good way to do it. Much of the policy debate in Washington has centered over who should shoulder the costs, but you can't make them go away. And until they are dealt with, they will act as a drag on the economy.

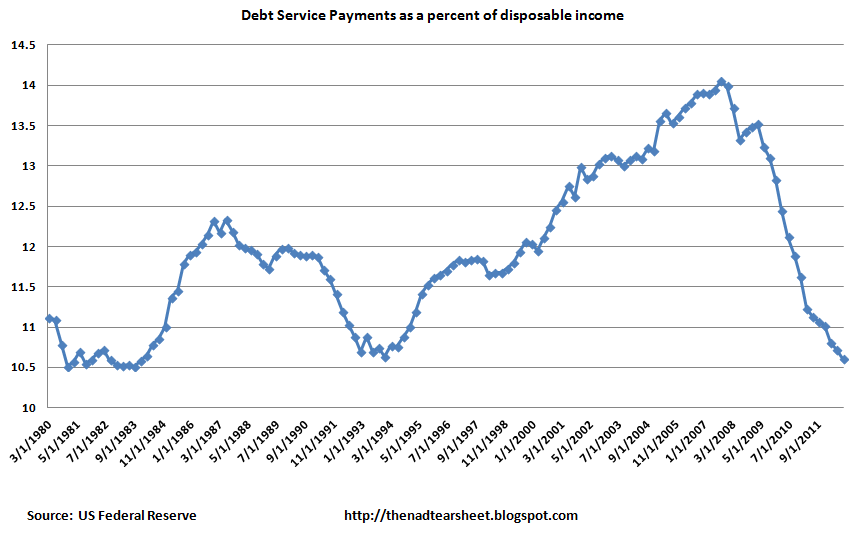

Luckily, corporate America is awash in cash. They are done deleveraging. The banks are still working their way through it, and no one really knows where they are marking some of their dodgier paper. Households are a mixed bag. Debt service (the amount of principal and interest payments) is at multi-decade lows, however the total amount of debt is not. We have some ways to go here. The recovery will be made on two fronts - debt will be slowly paid down, while real estate prices will continue to rise. And that is why the Fed is doing QE - to (officially) cut down debt service payments, and to (unofficially) help goose the real estate market.

Chart: US Household debt as a percent of GDP:

Chart: Debt Service Payments as a multiple of disposable income

But ZIRP and QE isn't "free." Unintended consequence of ZIRP # 547,624 - a bubble in student loan paper. Sallie Mae just sold $1.1 billion of securities backed by private student loans (in other words, not backed by the Federal Government) and the riskiest tranches were 15x oversubscribed. This year alone, dealers sold $5.6 billion of student loan backed securities, with an average yield of 1.48%. And we have only issued about a billion dollars worth of jumbo securitizations since the bubble burst? I find it absolutely amazing that we can securitize unsecured loans made to students majoring in underwater basket weaving, but we can't securitize a stated income loan. Is it Dodd-Frank and its open questions regarding "skin in the game" for issuers? If it is, I suspect the private label market will come back in a hurry once the regulators figure out what they want to do.

No comments:

Post a Comment