| Last | Change | |||

| S&P futures | 2609 | 5 | ||

| Eurostoxx index | 370.62 | 1.36 | ||

| Oil (WTI) | 64.88 | -0.37 | ||

| 10 Year Government Bond Yield | 2.77% | |||

| 30 Year fixed rate mortgage | 4.45% | |||

Stocks are higher this morning on end of month / quarter window dressing. Bonds and MBS are up.

Stocks are set to break a 9 quarter winning streak. The market leaders - the FAANG stocks - have been taking a beating as Facebook gets hit on data issues, and Amazon finds itself in the Administration's doghouse.

The bond market will close early today, at 2:00 pm EST. Get your locks in early, as secondary marketing types will probably build in a margin cushion to protect themselves over the long weekend.

Personal Income rose 0.4% in February, while personal spending rose 0.2%. The Personal Consumption Expenditure Index rose 0.2% MOM and 1.8% YOY. The core PCE index (the Fed's preferred measure of inflation) was up 0.2% MOM and 1.6% YOY. The core PCE numbers were a touch higher than the Street was looking for, and everything else was in line. The savings rate rose. Bonds are rallying a bit on the report.

Initial Jobless Claims fell to 215,000 last week, barely missing the late February number of 210,000. We haven't seen these levels since the early Carly Simon's "Your'e So Vain" topped the charts. When you take into account population growth the number is even more dramatic.

The FHFA announced that Fannie and Freddie will be issuing a new uniform mortgage backed security beginning in June of 2019. "The transition to the new, common security requires planning, investment, and preparation by a wide variety of market participants," said FHFA Director Melvin L. Watt. "We have now set the specific date that the Enterprises will start issuing the UMBS and I urge the industry to get ready now to ensure smooth, successful implementation." This will help bring Fannie and Freddie pricing more in line with each other.

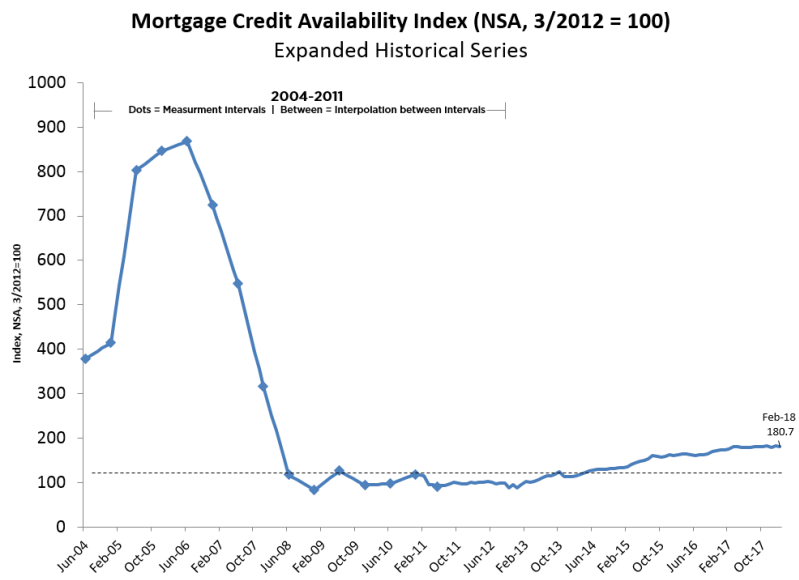

Is fintech reaching parts of the market that have not been fully served by traditional banks and lenders? The Philly Fed finds some evidence that it does, particularly in areas where there is high lender concentration (i.e. only a few banks) and areas that don't have much in the way of banks.

Barclay's Bank agreed to pay $2 billion in civil penalties to settle an investigation concerning RMBS issued during the bubble years. “In general, the borrowers whose loans backed these deals were significantly less credit-worthy than Barclays represented,” the Justice Department said in a statement Thursday. Barclay's had committed to keep the settlement under $2 billion in 2016, but the Obama Justice Department balked.

A Reuters poll of 75 bond strategists suggests that fears of oversupply in the Treasury market are overblown. They are looking for an increase of 40-50 basis points in the 10 year bond yield in 2018. Considering that we are already up 30 basis points this year, we probably aren't looking at major increases from here - maybe we will find a range of 2.8% to 3% and bounce around.