| Last | Change | |||

| S&P futures | 2719 | -3.75 | ||

| Eurostoxx index | 374.05 | -1.52 | ||

| Oil (WTI) | 63.42 | 1.36 | ||

| 10 Year Government Bond Yield | 2.90% | |||

| 30 Year fixed rate mortgage | 4.46% | |||

Stocks are lower as we await the FOMC decision. Bonds and MBS are down.

The FOMC decision is scheduled to be released at 2:00 pm EST. This will be Jerome Powell's first rate hike and press conference, so the markets will be hanging on his every word. Here are some of the things the Street will be focusing on. The biggest will be the dot plot for the rest of the year. Do the tax cuts and planned infrastructure spend push the Fed to bump up their consensus of 3 hikes this year to 4%? If so, that is bearish for bonds (higher rates). Another will be the long term neutral Fed Funds rate, which currently stands at 2.8%. Do they move it up to 3%? That sort of revision would be taken as hawkish as well and would push rates higher. Finally, the long-term unemployment rate is currently set at 4.6%, which implies the current rate of 4.1% is too low. If they move down the longer-term unemployment rate, that could be interpreted as dovish.

While most mortgage market participants are rightly focused on the 10 year bond yield, there is another rate that is gathering attention - LIBOR. LIBOR has been rising steadily over the past 18 months, and and 3-month LIBOR is at levels not seen since 2008. LIBOR and the 1 year T-bill rate are the reference index in many adjustable rate loans. What does this mean for the mortgage industry? Funding costs are rising, while volumes are falling. Not a good mix for profitability. Also note that this is yet another reason for borrowers with ARMs to consider a refi into a 30 or 15 year fixed rate mortgage. Long-term rates have been much more stable than LIBOR, and therefore the relative attractiveness is increasing.

Note that increasing short-term rates are having a spill-over effect onto other asset classes. Long-term bonds have had no competition from money market instruments for a decade. That is changing.

Mortgage Applications fell 1% last week as purchases rose 1% and refis fell 5%.

Existing home sales rose 3% in February to a seasonally adjusted pace of 5.54 million. This is up 1.1% YOY. The median home price rose 5.9% to $241k. Total housing inventory stood at 1.59 million, which is 8% lower than a year ago. The first-time homebuyer accounted for 29% of sales, which is down from 31% a year ago, and well below the historical average of 40%. Days on market fell to 37. The average contract rate for a 30 year mortgage increased 3 basis points to 4.33%. Distressed sales fell to 4%. Overall, it is the same story - tight inventory and rising prices.

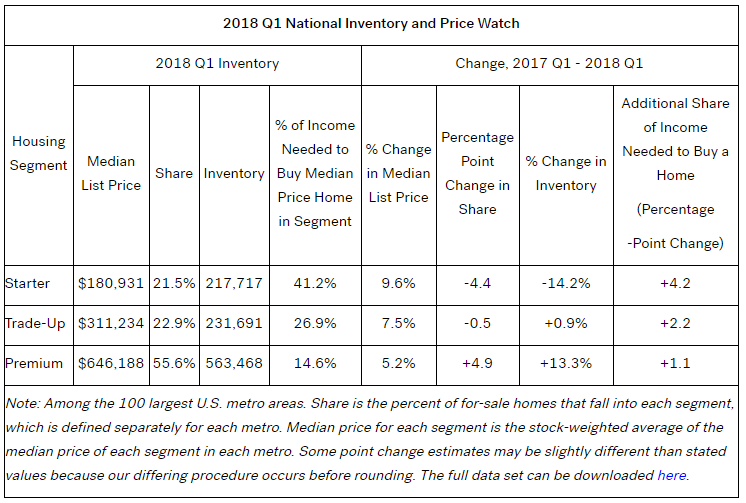

For the first time homebuyer, this is bad news, as most of the inventory is at the high end, not the low end. Starter homes in the Bay Area are over $800k, and engineers in Silicon Valley are struggling to pay the rent. Starter homes account for 22% of the inventory, while luxury accounts for almost 60%.

Meanwhile, construction job openings are the approaching post-recession highs. Lack of labor remains the biggest issue for construction companies.

Congress seems close to a deal to keep the government open after funding expires on Friday. Fiscal conservatives will be unhappy, as the trade seems to be higher military spending for higher non-military spending. For originators, the biggest issue with a government shutdown is the inability to get 4506-T reports out of the IRS.

No comments:

Post a Comment