| Last | Change | |||

| S&P futures | 2652 | 0.25 | ||

| Eurostoxx index | 387.17 | 2.14 | ||

| Oil (WTI) | 67.45 | 0.19 | ||

| 10 Year Government Bond Yield | 2.99% | |||

| 30 Year fixed rate mortgage | 4.55% | |||

Stocks are flat as we await the FOMC decision. Bonds and MBS are down small.

Mortgage Applications fell 2.5% last week as purchases fell 2% and refis fell 4%.

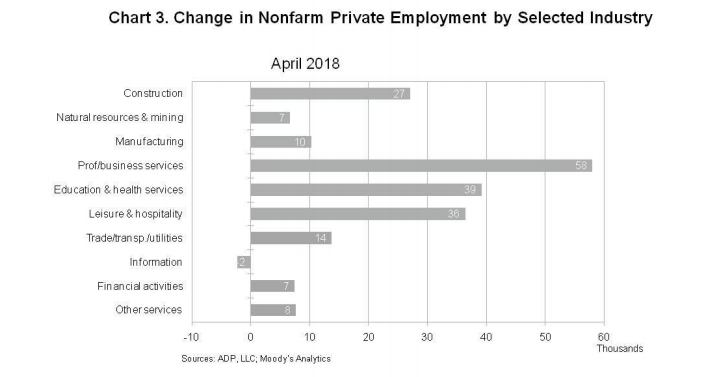

The economy added 204,000 jobs last month according to the ADP Employment Report. This was higher than expectations and is above the Street estimate for Friday's jobs report. Medium sized firms (50-500 employees) added the most jobs, and Professional and Business Services sector had the most growth. Construction added a lot of jobs as well.

The FOMC announcement is scheduled for 2:00 pm EST today. No changes in rates are expected, but investors will be looking to see if the Fed changes its language about inflation running below target. The latest PCE index came in at 2%, which is the Fed's target. The second-order question will be to see whether the Fed changes their 2% rate from a symmetric target to a ceiling. The most likely outcome will be a "steady as she goes" statement and any changes will be communicated at the June meeting with a fresh set of economic forecasts. Today's announcement should be a nonevent.

The Fed Funds futures are predicting a 6% chance of a hike at the May meeting and a 94% chance of a 25 basis point hike at the June meeting.

The labor shortage is so acute in the Rust Belt that some towns are paying people to move there. Most of these small towns have a major demographic problem - younger workers moved to the cities in response to the Great Recession, leaving only the older workers who are now retiring. The fear is that labor shortages will prompt employers to leave, which will create a downward spiral.

Consumer advocates worry that Mick Mulvaney is not going to blow up the CFPB, but will neuter it with a thousand cuts. That said, the rhetoric from the left is a bit overblown. Mick Mulvaney said: “When I took over, we had roughly 26 lawsuits ongoing,” he told the House Appropriations Committee on April 18. “I dismissed one, because the other 25 I thought were pretty good lawsuits.”

Consumer advocates worry that Mick Mulvaney is not going to blow up the CFPB, but will neuter it with a thousand cuts. That said, the rhetoric from the left is a bit overblown. Mick Mulvaney said: “When I took over, we had roughly 26 lawsuits ongoing,” he told the House Appropriations Committee on April 18. “I dismissed one, because the other 25 I thought were pretty good lawsuits.”