| Last | Change | Percent | |

| S&P Futures | 1377.0 | 2.1 | 0.15% |

| Eurostoxx Index | 2359.4 | -33.1 | -1.38% |

| Oil (WTI) | 102.05 | -0.4 | -0.40% |

| LIBOR | 0.4692 | 0.000 | 0.00% |

| US Dollar Index (DXY) | 79.863 | 0.130 | 0.16% |

| 10 Year Govt Bond Yield | 2.05% | 0.00% | |

| RPX Composite Real Estate Index | 170.57 | 0.0 |

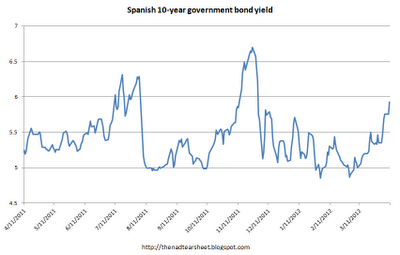

Markets are generally weaker as Europe plays catch-up with the US markets. US bonds and MBS are flat. Spanish yields are 17 basis points higher on no major economic news. An unexpected drop in imports pushed the Chinese trade balance into a surplus and is flashing warning signs about Chinese domestic demand.

With Greece temporarily off the front pages, all eyes turn to Spain. The new Spanish government is determined to implement austerity measures and reduce the budget deficit by almost 2/3 in 2013. Spain had a massive property bubble, which has weakened their banking system considerably. The banks are thought to be marking their real estate portfolios and mortgage bonds at unrealistic levels.

One powerful method of clearing the excess housing inventory is the short sale, and often times it is a lengthy, painful process as banks and other creditors drag their feet, hoping for better prices. Senator Sherrod Brown (D-OH) has introduced legislation to force banks to make a decision within 75 days of a request from a homeowner.

Bloomberg has been tracking a story about J.P. Morgan's massive credit default swap positions in their Treasury department, which is raising questions about Dodd-Frank and proprietary trading versus hedging. The trader, Bruno Iksil, has been selling protection on an index of investment-grade bonds (Markit CDX North America Investment Grade Series 9) and is thought to have sold $100 billion worth of protection on the index. This is the trade that blew up AIG and I cannot imagine what it possibly could be hedging. As a bank, JP Morgan generally makes loans so it makes money if US corporations generally do well, and poorly when US corporations don't do well. Selling protection is the exact same bet. The article goes on to speculate that this may be part of a spread trade, but even then a spread trade is a speculative position, not a hedge. Anyway, regulators and politicians seem to be lining up against this trade, and if JP Morgan is forced out, they will undoubtedly pay dearly to exit.

Chart: Spanish 10-year government bond yields

No comments:

Post a Comment