| Last | Change | |

| S&P Futures | 2261.2 | 1.2 |

| Eurostoxx Index | 360.5 | 0.5 |

| Oil (WTI) | 52.2 | 0.1 |

| US dollar index | 93.4 | 0.2 |

| 10 Year Govt Bond Yield | 2.56% | |

| Current Coupon Fannie Mae TBA | 103 | |

| Current Coupon Ginnie Mae TBA | 104 | |

| 30 Year Fixed Rate Mortgage | 4.29 |

Stocks are flattish this morning on no real news. Bonds and MBS are up small.

Expect a dull week with thin volume on the exchanges as many traders take this week off. We will have some minor economic reports this week, but nothing should be market-moving.

New Home Sales increased to 592k in November. This is an increase of 17% YOY. New home inventory is about 250k, which is a 5.1 month supply at current levels. The median sales price was $305k, while the average sales price was $359k. The Midwest and the West had the biggest increases in sales.

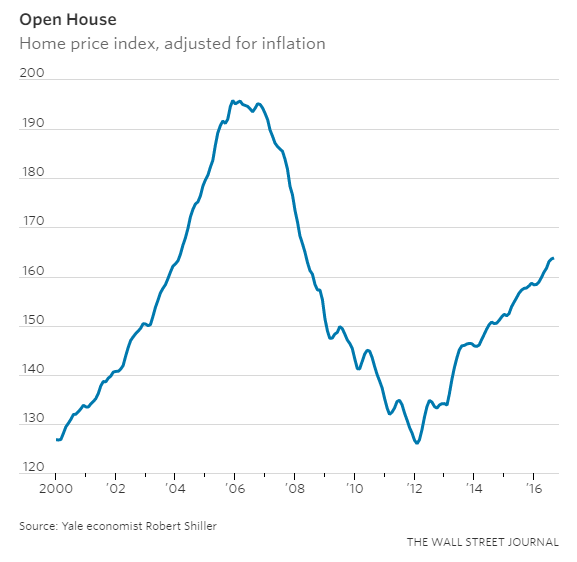

Home prices rose 5.6% in October, according to the Case-Shiller Home Price Index. Affordability measures have shown 20% - 30% decreases since home prices bottomed in 2012. While affordability is not yet at a point to suggest a reversal in home price appreciation, we are probably approaching the limits of home price appreciation unless wage growth accelerates.

Note that these indices are not inflation-adjusted. While inflation has been pretty tame over the past 10 years, it hasn't been zero. If you adjust the index for inflation, we are still below our 2006 highs.

The national foreclosure inventory fell below 500k for the first time in 10 years, according to Black Knight Financial Services. Delinquencies ticked up on a seasonal basis, but are down almost 10% YOY. Improvements in delinquencies are getting smaller as the market normalizes.

For bond investors who were taken by surprise by the Fed's forecast of 3 rate hikes this year, it is instructive to look at how many hikes they thought they would be making this year. In fact, no one suggested less than 2. We only had one. This again stresses the data-dependency of what the Fed is thinking. GDP growth came in slower than expected, and then we had Brexit, which caused the Fed to think about being less aggressive. Ultimately, it will depend on inflation and whether it returns. Despite inflation being below the Fed's target rate, they still plan to tighten.

Consumer confidence jumped in November, driven primarily by the election and improving expectations for future growth. Note that the current conditions part of the index actually fell, so this is largely a jump based on the perception of the future which may not play out as assumed.

No comments:

Post a Comment