| Last | Change | Percent | |

| S&P Futures | 1996 | -16.2 | -0.78% |

| Eurostoxx Index | 3141 | -63.0 | -1.73% |

| Oil (WTI) | 35.7 | 0.04 | -0.76% |

| LIBOR | 0.492 | 0.006 | 1.13% |

| US Dollar Index (DXY) | 97.77 | -0.165 | -0.17% |

| 10 Year Govt Bond Yield | 2.17% | 0.04% | |

| Current Coupon Ginnie Mae TBA | 104.4 | ||

| Current Coupon Fannie Mae TBA | 103.4 | ||

| BankRate 30 Year Fixed Rate Mortgage | 3.93 |

Markets are lower this morning as oil continues to fall and problems at a high yield mutual fund begin to spill over.

No economic data today. The markets will be focused on the Fed and the evolving situation in distressed debt markets.

No economic data today. The markets will be focused on the Fed and the evolving situation in distressed debt markets.

Marty Whitman's Third Avenue Focused Credit Fund has suffered losses as the rout in high yield has reduced liquidity. Dodd-Frank has severely curtailed market-making operations at investment banks, and right now there are very few buyers of distressed credit as hedge funds face redemptions and investment banks cannot step in because of capital requirement. In fact, the regulators are considering additional steps to ensure a bank failure doesn't bring down the entire financial system, which means that investment banks will probably de-risk further, making them even less likely to act as market-makers. This will be an interesting first test of a financial crisis in the new Dodd-Frank world.

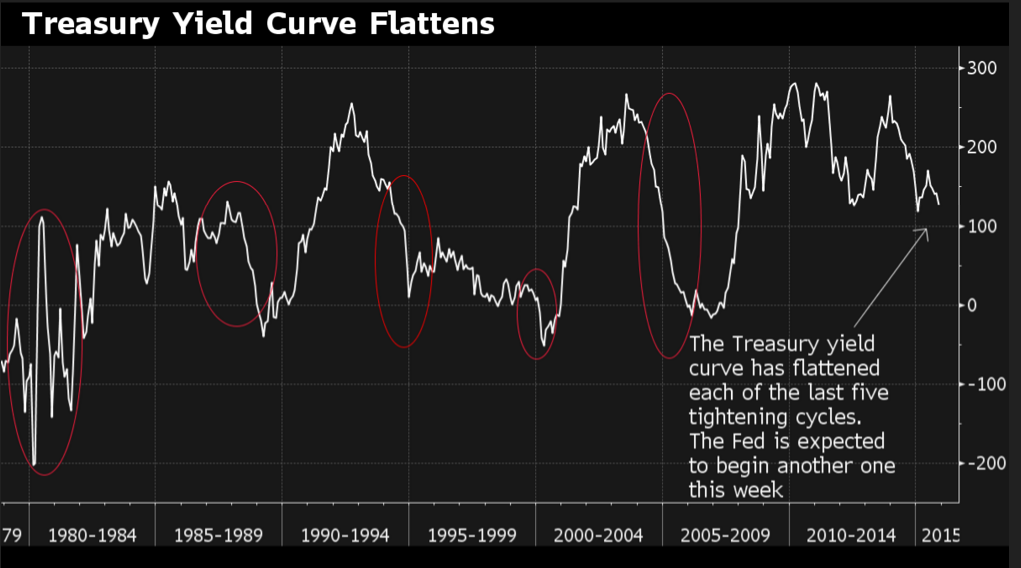

As a general rule, in credit crunches, the long bond rallies. You saw that on Friday, where the 10 year yield fell 10 basis points in spite of strong retail sales data. This week will be interesting between the evolving Third Avenue situation and the FOMC decision on Wednesday. LOs, expect bond market volatility this week. As a general rule, tightenings have not had a dramatic effect on mortgage rates. In fact, the yield curve has flattened during all the tightening cycles since 1979. Granted, these tightenings have taken place in context of a secular bull market in bonds, so take this analysis with a grain of salt. That said, unless the economy really starts taking off (and you start seeing wage inflation), chances are that the 10 year yield increases less than the amount of the rate hike. Note that CoreLogic is forecasting a 4.5% 30 year fixed rate mortgage by the end of 2016.

Mortgage loan performance has been improving, according to the OCC. Performing loans increased to 93.9% from 93% a year earlier. New foreclosures are down 22% YOY.

Ex GMAC Ally Financial is getting back in the mortgage business. Ally CEO said this about the move: “Don’t think of this as Ally going down the road of the old GMAC,” Brown said, referring to the home lending unit that brought Ally to the brink of collapse. The ironic thing is that the "new subprime" is auto loans, and that is Ally's bread and butter these days. They are offering 8 year loans for new cars at rates at rates substantially below the 30-year fixed rate mortgage (think 3.5% range). Given that new cars depreciate like sushi, this is a very, very mispriced loan. If you are wondering why the Fed wants to get off the zero bound even in the face of zero inflation, there you go. Those sort of rates are a function of ZIRP and the impossibility of earning a decent rate of return. It would be ironic if the ne-er do well of mortgages had simply morphed into the ne-er to well of auto lending and we see a collapse in asset backed security liquidity.

As a general rule, in credit crunches, the long bond rallies. You saw that on Friday, where the 10 year yield fell 10 basis points in spite of strong retail sales data. This week will be interesting between the evolving Third Avenue situation and the FOMC decision on Wednesday. LOs, expect bond market volatility this week. As a general rule, tightenings have not had a dramatic effect on mortgage rates. In fact, the yield curve has flattened during all the tightening cycles since 1979. Granted, these tightenings have taken place in context of a secular bull market in bonds, so take this analysis with a grain of salt. That said, unless the economy really starts taking off (and you start seeing wage inflation), chances are that the 10 year yield increases less than the amount of the rate hike. Note that CoreLogic is forecasting a 4.5% 30 year fixed rate mortgage by the end of 2016.

Mortgage loan performance has been improving, according to the OCC. Performing loans increased to 93.9% from 93% a year earlier. New foreclosures are down 22% YOY.

Ex GMAC Ally Financial is getting back in the mortgage business. Ally CEO said this about the move: “Don’t think of this as Ally going down the road of the old GMAC,” Brown said, referring to the home lending unit that brought Ally to the brink of collapse. The ironic thing is that the "new subprime" is auto loans, and that is Ally's bread and butter these days. They are offering 8 year loans for new cars at rates at rates substantially below the 30-year fixed rate mortgage (think 3.5% range). Given that new cars depreciate like sushi, this is a very, very mispriced loan. If you are wondering why the Fed wants to get off the zero bound even in the face of zero inflation, there you go. Those sort of rates are a function of ZIRP and the impossibility of earning a decent rate of return. It would be ironic if the ne-er do well of mortgages had simply morphed into the ne-er to well of auto lending and we see a collapse in asset backed security liquidity.

No comments:

Post a Comment