| Last | Change | |

| S&P Futures | 2338.5 | -7.0 |

| Eurostoxx Index | 368.5 | -1.6 |

| Oil (WTI) | 53.1 | -0.3 |

| US dollar index | 910.9 | 0.1 |

| 10 Year Govt Bond Yield | 2.41% | |

| Current Coupon Fannie Mae TBA | 102.1 | |

| Current Coupon Ginnie Mae TBA | 103.2 | |

| 30 Year Fixed Rate Mortgage | 4.11 |

Stocks are lower this morning on overseas weakness. Bonds and MBS are up.

The index of leading economic indicators rose 0.6%, stronger than expected.

Household debt increased in the fourth quarter, as growth in non-mortgage debt outpaced growth in mortgage debt. The 4th quarter saw $617 billion in newly originated mortgages, the highest level since Q32007. Auto loans and student loans saw an uptick in 90 day delinquencies, while credit cards and mortgages saw an improvement. Remember, this is only the debt side of the equation - both incomes and asset prices (especially housing) are higher than they were in 2007.

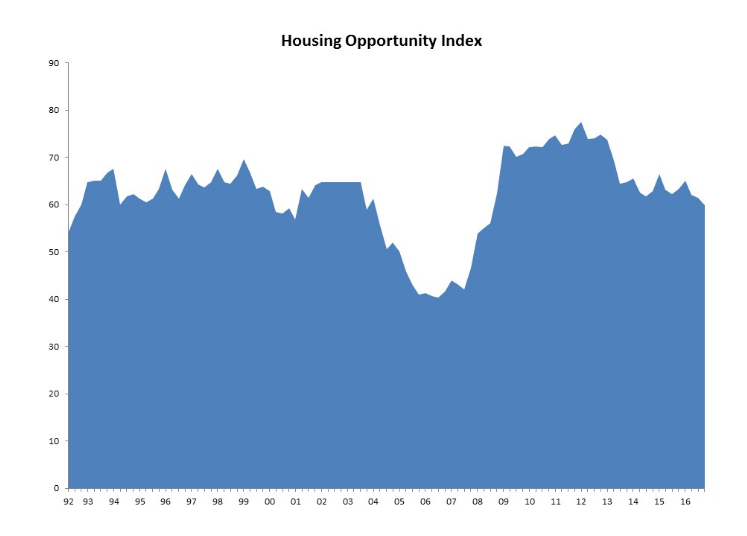

Housing affordability remains about in line with pre-crisis levels, according to the NAHB. As of the end of the year, approximately 59.9% of all homes were affordable to a borrower with the median income. You can see the big swing in affordability between the boom and bust years. Tight inventory is being offset by (still) low mortgage rates. California remains the biggest issue regarding affordability. In the San Francisco MSA, just 7.8% of the homes sold were affordable to people earning the median income of $104,700.

The median home price increased 7% in January to $261,100, according to Redfin. Home sales were up 5.6% compared to January 2016, which shows that the uptick in rates hasn't affected the purchase market. Inventory is down 12% YOY, and listings have dropped 5.1%. 18% of homes sold above list price, and the average sales to list ratio was 93.7%. Days on market fell 7 days YOY to 59.

Despite all the missteps of the initial days of the Trump administration, stocks are partying like it is 1999. This certainly has the political class (and the business press) scratching their heads. First, while the first 100 days of the Official U.S. Airing of The Grievances may seem dramatic, it doesn't mean much for business (except for some consumer product companies and retailers who suffer from ideologically-driven boycotts). Second, for all the talk in the business press of "uncertainty," investors are sensing (correctly, I think) that gridlock is going to rule the day in DC. Nothing is more "certain" than gridlock, and if regulations get eased a bit, that is good for business. Gridlock also means the Fed has some room to go slower. At the end of the day, earnings drive the stock market, not the histrionics in Washington and the media.

No comments:

Post a Comment