| Last | Change | Percent | |

| S&P Futures | 1394.3 | -6.3 | -0.45% |

| Eurostoxx Index | 2418.2 | -18.8 | -0.77% |

| Oil (WTI) | 91.79 | -1.6 | -1.68% |

| LIBOR | 0.437 | -0.001 | -0.11% |

| US Dollar Index (DXY) | 82.8 | 0.157 | 0.19% |

| 10 Year Govt Bond Yield | 1.63% | -0.06% | |

| RPX Composite Real Estate Index | 189.1 | 0.1 |

Stocks are taking a breather this morning after a 6-day rally. Chinese and French economic data showed that their respective economies are slowing. Import prices fell 3.2%. Bonds are up 27 ticks and MBS are up about a quarter of a point.

The USDA cut its corn production forecast 17% due to the drought, while corn has rallied 63% in the last two months. Since corn is also used for feed and is a big input into other foods, price increases will flow through to other foods as well. So if you were wondering why you are spending so much more on groceries (which is our 2nd biggest expenditure after shelter) now you know why. Gas isn't the only commodity that can influence consumer behavior.

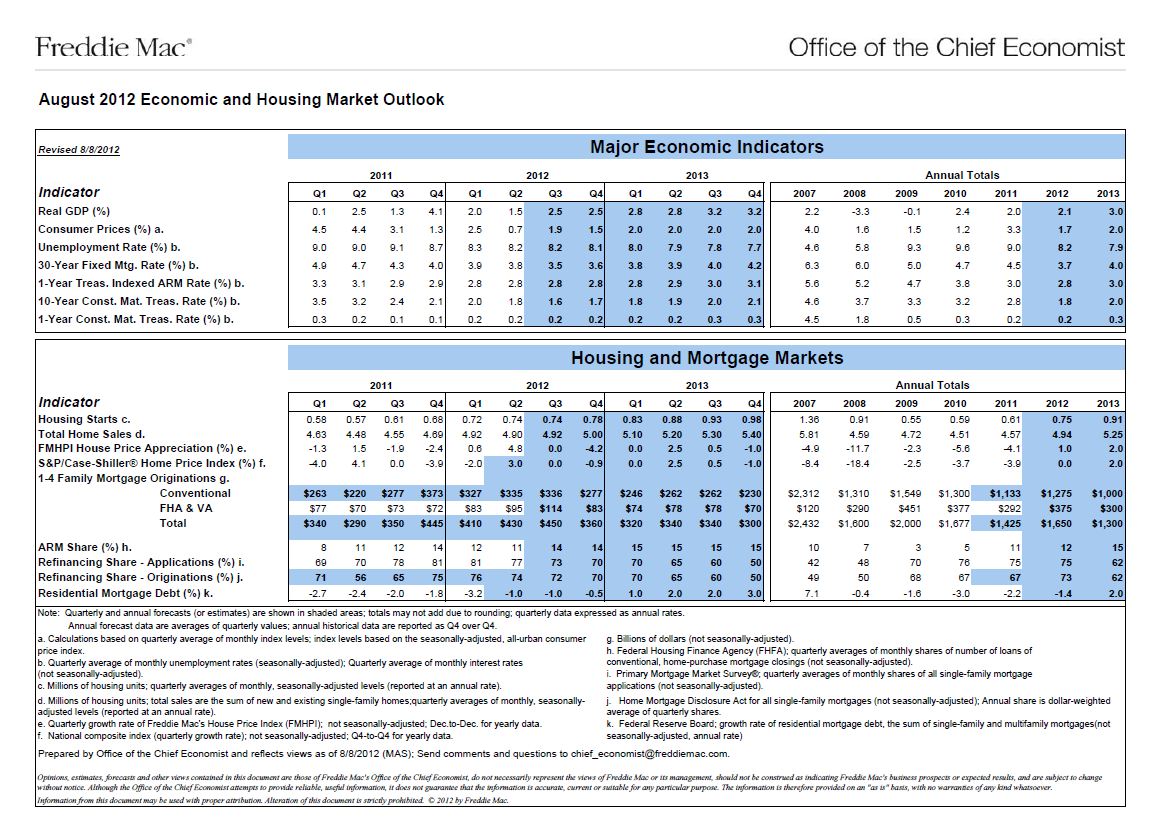

The debate going on regarding house prices centers on this: Bull Case: Housing has never been more affordable, prices appear to have bottomed and are increasing. Bear Case: Price Increases are due to constricted supply and once the shadow inventory hits the market back down we go. Freddie Mac Chief Economist Frank Nothaft examines the issue in the latest Freddie Mac US Economic and Housing Market Outlook. His conclusion is that the shadow inventory is still there, but it has been dramatically reduced. I tend to agree, although there isn't really a standard definition of "shadow inventory." Certainly the red-hot rental market is attracting professional investors, while boomerang college grads are crimping supply. As a trader, my take is that after 6 years, whatever inventory is left is largely in strong hands. I don't see a capitulation trade happening. I do find his economic forecasts to be way aggressive, though. He is predicting 2.5% GDP growth through the end of the year, with 2.8% in Q113 and 3.2% in Q213 and mortgage rates gradually ticking up to 4.2% by the end of 2013. Mortgage origination volumes are set to fall as the refinancing boom runs its course. You can click on the table below to increase the size.

No comments:

Post a Comment