Stocks are flat this morning after GDP came in better than expected. Bonds and MBS are down small.

Mortgage Applications fell 1.7% last week as purchases fell 1% and refis fell 3%. This is despite a drop in rates.

Second quarter GDP was revised upward to 4.2% from 4.1%, which was higher than the street estimate of 4.0%. The main revisions were to consumption (downward) and fixed residential investment (upward). Inventories were a drag on GDP, which means that we should see a bump to Q3's numbers. The GDP price index was also revised up a touch, from 1.8% to 1.9%. All of this provides a good environment for the Fed to ease back from the zero bound.

Mortgage bankers made $580 per loan in the second quarter, an increase from $118 in the first quarter. Banks cut costs aggressively (dropping production costs per loan by about $1,000) however declining volumes offset that, and this turned out to be the weakest quarter since the MBA began keeping records in 2008. That $580 represents a profit of 21 basis points per loan, which was a drop form 24 bps a year ago. Fee income dropped to 341 bps from 370 in the first quarter. Refis continue to decline, with purchases accounting for 81% of all volume.

Here is something wild. Last night, there were no trades in the JGB market (the world's second largest bond market). This is the 7th time this has happened this year. The Bank of Japan basically controls the market, and trading has dried up. We live in interesting times, at least if you are a central banker.

Pending Home sales fell 0.7% in July, according to NAR. Lawrence Yun, NAR chief economist, says the housing market’s summer slowdown continued in July. “Contract signings inched backward once again last month, as declines in the South and West weighed down on overall activity,” he said. “It’s evident in recent months that many of the most overheated real estate markets – especially those out West – are starting to see a slight decline in home sales and slower price growth.” Blame tight supply, which has driven up prices to unaffordable levels.

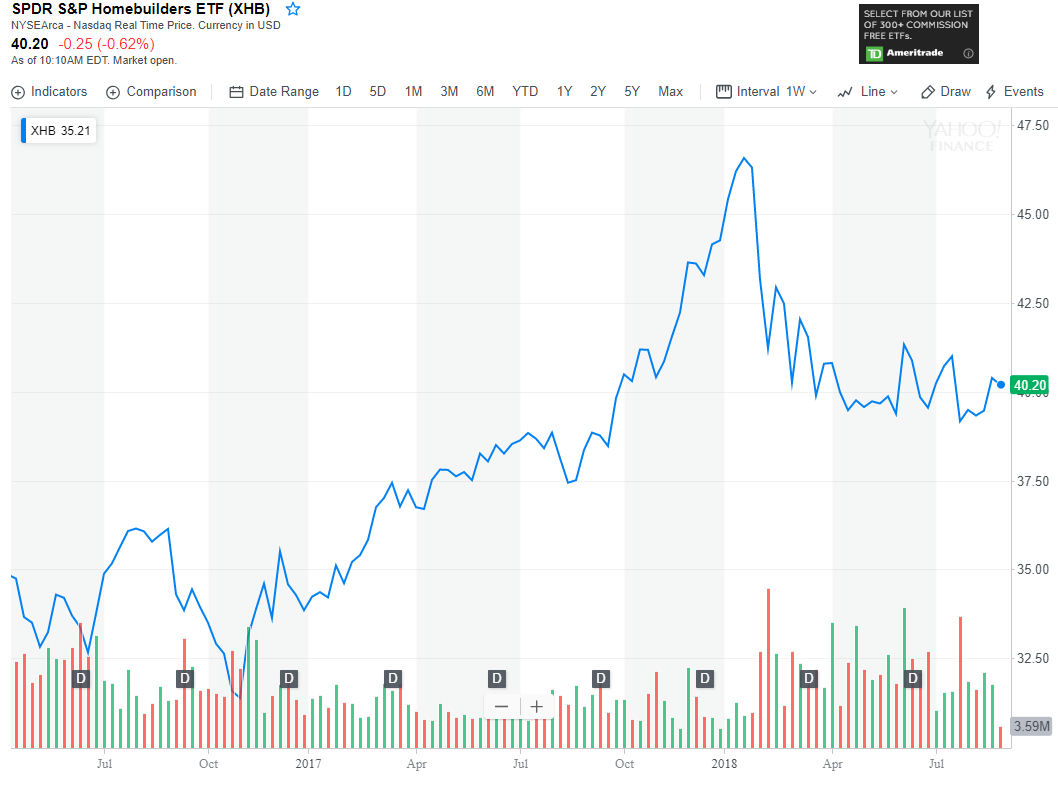

The housing slowdown has not been lost on the stocks of the homebuilders, who despite strong earnings (and an incredibly strong stock market) are down 14% YTD. At some point, the sector will be unable to rely on increasing ASPs and will have to pump up volume to show growth. Despite the clear need for new housing, especially at the starter level, builders seem content to meter their growth and plow excess cash into buybacks.

No comments:

Post a Comment