| Last | Change | |||

| S&P futures | 2862 | 4 | ||

| Eurostoxx index | 384.93 | 1.7 | ||

| Oil (WTI) | 67.47 | 1.04 | ||

| 10 Year Government Bond Yield | 2.83% | |||

| 30 Year fixed rate mortgage | 4.58% | |||

Stocks are higher this morning as earnings season winds down. Bonds and MBS are down.

Same store sales rose 4.7% last week, which is indicative of a strong back-to-school shopping season. BTS is a good predictor of the holiday shopping season, which would support strong GDP growth for the rest of the year. Consumption is about 70% of US GDP. Current projections are looking at north of 3% growth for the year.

The Fed Funds futures are now handicapping a 96% chance of a Sep hike and a 63% chance of a Sep and Dec hike. Meanwhile, the yield curve continues to flatten.

Trump made some comments about Fed Chairman Jerome Powell at a fundraiser, saying that he expected him to be a "cheap money guy" and didn't expect him to raise interest rates. He also tweeted that he is "getting no help" from the Fed. While publicly discussing monetary policy is not a normal thing for the President to do, wishing rates were lower is. The only politicians who want higher rates are the ones not in power. He also called the Europeans and the Chinese currency manipulators. Under any other President this would be big, but the dollar and the bond market largely ignored it. It shows that markets are largely dismissing "Donald being Donald" communiques from the WH.

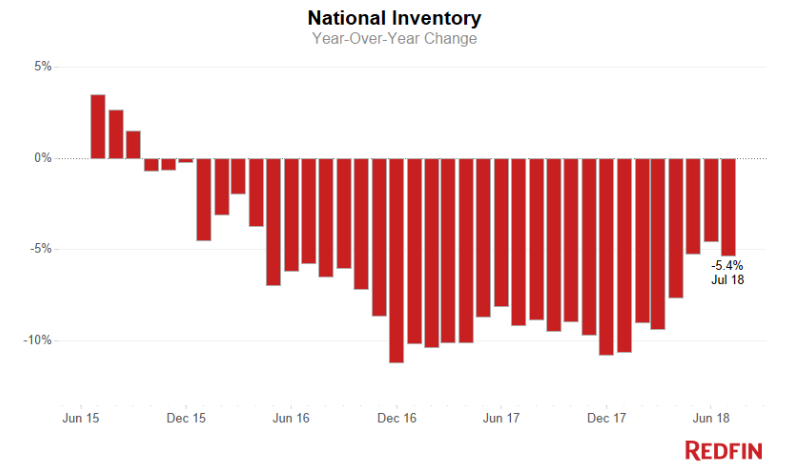

The YOY declines in inventory that have bedeviled the industry are beginning to moderate, at least according to Redfin. Inventory was down 5.8% in July, which is lower than the double-digit decreases we had been seeing. The median sales price rose 5.3%. Homes went under contract in 35 days, which is 3 days faster than a year ago. Activity is slowing in some of the hotter markets however, especially Washington DC. The inventory issue won't be fixed until we get housing starts back to some semblance of normalcy, which means a few years of 2MM units before returning to historical averages of around 1.5MM.

Toll Brothers reported strong numbers this morning, which has sent the stock up 11%. Revenues were up 27% and deliveries were up 18%. Backlog rose 22% in dollars and 13% in units. They also bought back about $137 million worth of stock, which accounts for about 70% of earnings. Robert I. Toll, executive chairman, stated: “We believe there is room for continued growth in the new home market in the coming years. Household formations have been increasing and in many regions the aging housing stock may not satisfy the lifestyles of today’s buyers. Yet new home production has not kept pace with the growth in population and households. On the single-family side, housing starts, other than during the anemic years of this recovery, are at their lowest level since 1970. In addition, existing home values have increased, providing potential move-up and empty nester customers with more equity that they can put toward a new home purchase. We believe these two groups, along with the growing number of millennials starting to buy homes, are all sources of potential new demand in the coming years.”

I find it interesting that he talks about the low level of housing starts, while at the same time spending 70% of Toll's net income on buybacks. Certainly the actions don't seem to match the words.

No comments:

Post a Comment