| Last | Change | |

| S&P Futures | 2573.0 | 4.8 |

| Eurostoxx Index | 394.7 | 0.8 |

| Oil (WTI) | 54.1 | -0.1 |

| US dollar index | 87.6 | 0.1 |

| 10 Year Govt Bond Yield | 2.37% | |

| Current Coupon Fannie Mae TBA | 102.875 | |

| Current Coupon Ginnie Mae TBA | 103.938 | |

| 30 Year Fixed Rate Mortgage | 3.99 |

Stocks are up this morning as we start the November FOMC meeting. Bonds and MBS are down small.

No changes to FOMC policy are expected at this week's meeting, however the Fed Funds market is predicting a 96% chance they raise rates in December.

Aside from the FOMC meeting, Congress is expected to unveil tax reform tomorrow, and Trump is slated to nominate the new Federal Reserve Chairman on Thursday. And on Friday, we get the all-important jobs report, so a lot going on this week.

Despite what the business press is saying, the markets are treating the Mueller / Manafort thing as a sideshow. As of now, nothing going on there is going to affect Washington enough to rile up markets. Earnings are the focus at the moment for stocks, and economic data (along with foreign central bank policy) is driving the bond market.

The Washington DC goat rodeo isn't affecting consumer confidence either, which just hit a 17 year high. Most notably, the job market got positive marks for strength for the first time since 2001.

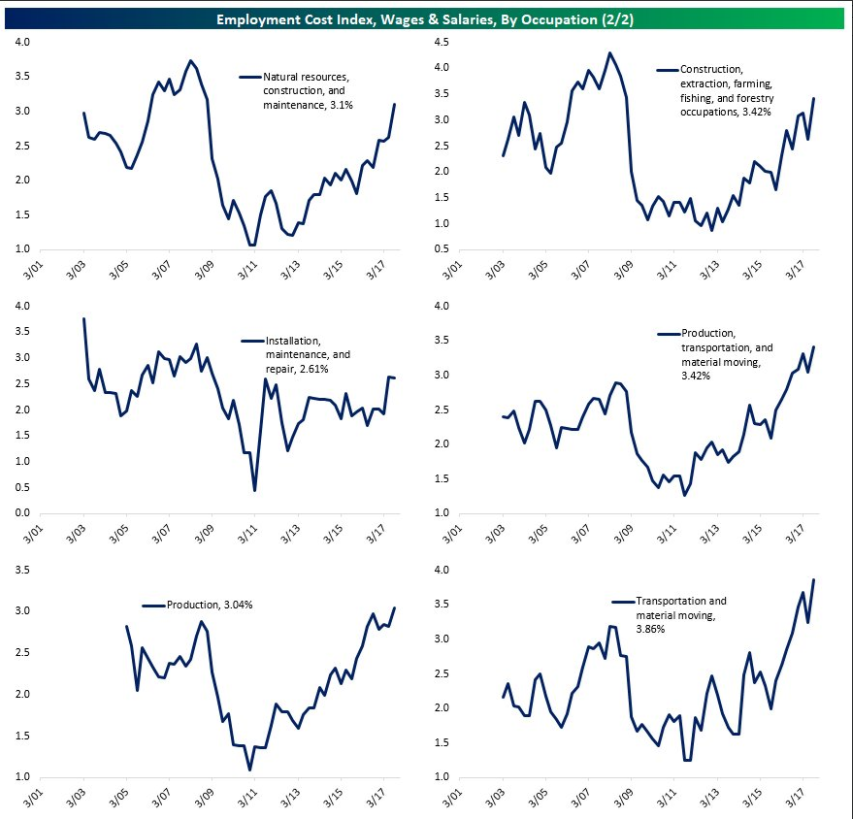

Are we starting to see stirrings of wage inflation? Perhaps. The Employment Cost Index rose 0.7% in the third quarter, faster than the 0.5% rate we saw in the second. Wages and salaries (which account for 70% of the ECI) rose 0.7%, while benefits rose 0.8%. On a year-over-year basis, they rose 2.5%. So far, bonds aren't reacting to the number. An increase in wage inflation will force the Fed to move more aggressively. For those who worry about income inequality, the biggest growth was in blue collar jobs, where wages rose 0.8% and benefits rose 1.7%.

Home prices rose 0.5% in August and are up 5.9% for the year, according to Case-Shiller. Seattle has been on a tear, rising over 13% for the past year, followed by Las Vegas and San Diego. A strong economy along with low inventory and rates have been a support for home prices. The interest rate environment will be changing, however inventory doesn't appear to be a temporary phenomenon, and the US economy seems to be accelerating, not declining. While the usual affordability questions are mentioned, the median mortgage payment for the median house as a percent of income is still very low by historical standards.

Note that the lack of building is simply creating pent-up demand for housing which will get satisfied eventually. That will push up growth for the next few years when it finally happens.

Manufacturing continues to hum along, with the Chicago PMI coming in well above expectations.

Bitcoin futures are coming... The contracts will be cash settled, not by delivery of the underlying.

No comments:

Post a Comment