| Last | Change | |

| S&P Futures | 2642.0 | 3.8 |

| Eurostoxx Index | 386.6 | -0.9 |

| Oil (WTI) | 57.3 | -0.2 |

| US dollar index | 86.7 | 0.1 |

| 10 Year Govt Bond Yield | 2.39% | |

| Current Coupon Fannie Mae TBA | 102.625 | |

| Current Coupon Ginnie Mae TBA | 103.625 | |

| 30 Year Fixed Rate Mortgage | 3.88 |

Stocks are higher this morning on no real news. Bonds and MBS are flat.

Toll Brothers announced earnings this morning that missed analyst expectations. The sector has been on a tear this year, so weak earnings are expected to be punished by the markets. Revenues increased 9% and earnings increased 68%. The company used a lot of its cash to repurchase stock and bonds, which isn't a great sign for future growth. Generally when companies are seeing great opportunities, they re-invest in the business. When they don't, they buy back stock. The street didn't like the guidance, and the stock is down about 6% pre-market.

Toll is in the luxury end of the housing market, covering McMansions in urban areas out West and luxury apartments in the East. The change in the mortgage interest deduction is probably going to impact demand. Note that the builders that focus on entry-level building are doing much better. For the past 10 years, the luxury end of the market was the only part that was working. Now the market is shifting to the first time homebuyer.

Speaking of the luxury end of the market, the New York Times frets about the effect tax reform will have on New York City. It turns out that 40,000 residents in New York City account for half the city's revenue. If they leave, it will have a huge impact on the city's finances. The people most affected will be those making over $200,000, and in a high cost area like New York City and the suburbs, that is not rich by any stretch of the imagination.

Factory orders fell 0.1% in October, ending a generally good month for manufacturing. Capital Goods orders were strong however, and that points to a stronger Q4 and 2018. Capital Goods orders are generally associated with business expansion, capacity increases, and modernization.

The services economy decelerated in November from a record in October, according to the ISM Non-Manufacturing Survey.

Tax reform heads to committee to resolve the differences between the House and Senate versions. Here are the biggest sticking points. The committee starts work on Monday, with an eye to have a final vote in Mid-December.

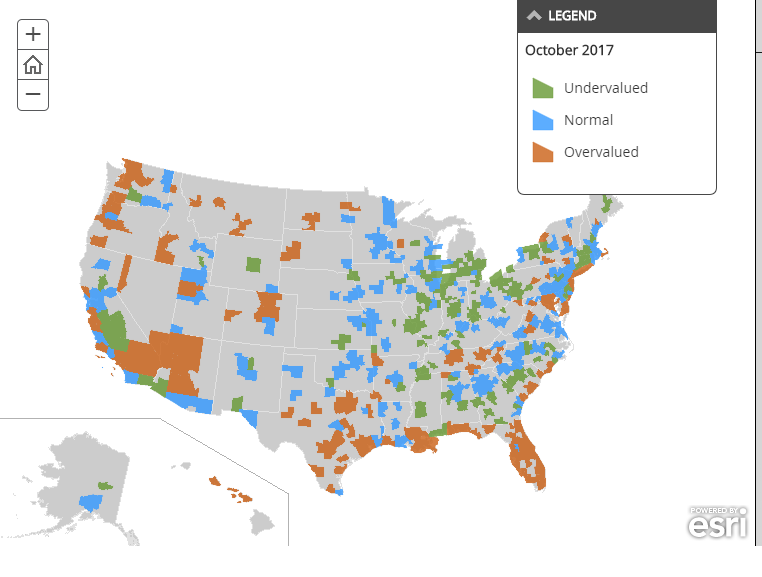

Home prices rose 0.9% MOM and are up 7% YOY, according to CoreLogic. The fastest growth continues to be in the West and Mountain states. Much of the Midwest remains undervalued while we are seeing overvaluation in places like Florida, Texas, and the West Coast. Note that fears about climate change are not evident in Florida real estate.

First time homebuyers are still relatively uninformed about mortgages. According to a recent survey, 20% of Americans think it is impossible to get a mortgage with less than 5% down, despite the fact that FHA goes down to 3%, VA allows nothing, and the GSEs have 3% down products. Most people get their information on the Internet, and surprisingly almost nobody gets their mortgage information from the CFPB.

How did HAMP and HARP help struggling homeowners? It turns out, not much. In fact, borrowers who had a principal reduction had pretty much the same default rates as borrowers without a principal reduction. These reductions were big: 32% or about $112,000 on average. These results pour cold water on the strategic default theory, which says that borrowers will choose to toss the keys to the bank once the home value is less than their outstanding mortgage. FWIW, I think the defaults in 2006 were strategic defaults, as the economy had yet to roll over and professionals were playing the greater fool game. Note that modifying a mortgage payment to a percentage of income didn't really help either. The punch line is that many defaults were caused by a short term blip in a borrower's financial situation - often an unexpected expense like a medical bill - and servicers should work on creating a solution to help the borrower over that hump and then re-evaluate.

No comments:

Post a Comment