| Last | Change | |

| S&P Futures | 2454.0 | 14.0 |

| Eurostoxx Index | 375.2 | 3.1 |

| Oil (WTI) | 48.7 | -0.2 |

| US dollar index | 86.2 | 0.2 |

| 10 Year Govt Bond Yield | 2.21% | |

| Current Coupon Fannie Mae TBA | 103.197 | |

| Current Coupon Ginnie Mae TBA | 104.068 | |

| 30 Year Fixed Rate Mortgage | 3.92 |

Stocks are higher this morning as tensions between the US and North Korea seemed to ease a bit over the weekend. Bonds and MBS are down.

Not a lot of data this week (nor is there any Fed-Speak). The highlight should be housing starts on Wednesday.

The St. Louis Fed is forecasting 3.7% GDP growth for Q3, while the Atlanta Fed is forecasting 4% growth. Seems surprisingly high, but we will get an idea of how realistic that is when retailers report same store sales for August, which covers the back-to-school shopping season.

These GDP forecasts (if they end up playing out) should boost rates higher over the near term. This will be offset by international tensions (and a general sense of uncertainty in DC) which will pull rates lower. There is no real way to forecast how things will shake out, but just be aware that this push-pull effect should make for increased rate volatility over the near term.

These GDP forecasts (if they end up playing out) should boost rates higher over the near term. This will be offset by international tensions (and a general sense of uncertainty in DC) which will pull rates lower. There is no real way to forecast how things will shake out, but just be aware that this push-pull effect should make for increased rate volatility over the near term.

With the Fed on hold until December, the markets are turning to the debt ceiling, which should hit in late September / early October. You are starting to see a tick up in the yields of 3 month T-bills maturing in late September. The debt ceiling has always been a bit of an annual kabuki dance, this time around the unpredictability of things in DC is making traders a little more worried.

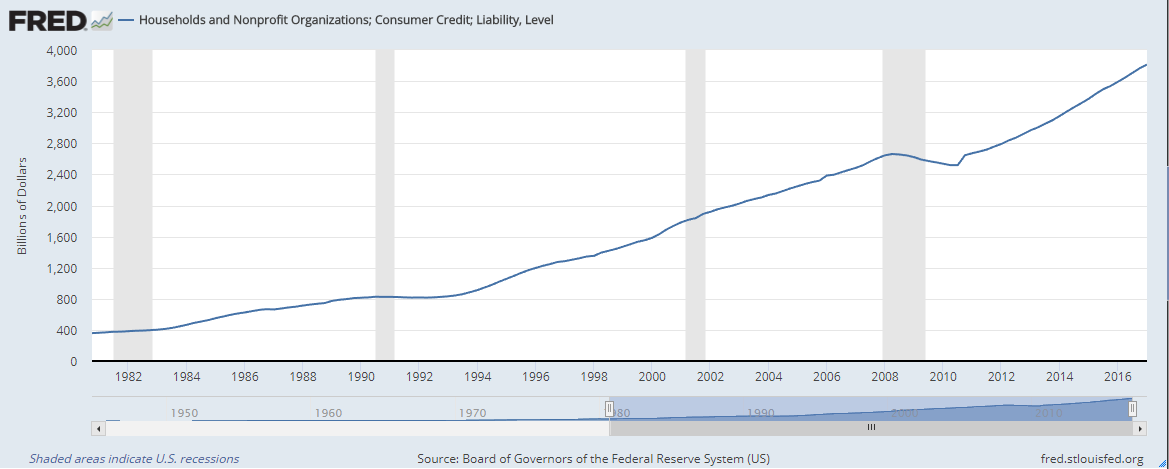

Average credit scores have eclipsed their October 2006 peak, hitting 700 this year. It is interesting to see that US consumer debt levels are at all-time highs, however debt service is at a low. Debt service is one's mortgage, car, installment, and credit card debt as a percentage of income. Check out the charts below:

Consumer credit:

Debt service:

These two charts demonstrate just how much interest rates matter (and why owning a home isn't quite as unaffordable as the home price indices suggest). If you want to see what determines how Fair Issac (of FICO fame) determines your score, here is a handy chart. The single best thing one can do is make timely payments, followed by reducing the amount they owe.

No comments:

Post a Comment