| Last | Change | Percent | |

| S&P Futures | 1999.2 | 2.5 | 0.13% |

| Eurostoxx Index | 3165.0 | 0.6 | 0.02% |

| Oil (WTI) | 95.03 | 0.5 | 0.51% |

| LIBOR | 0.235 | -0.004 | -1.47% |

| US Dollar Index (DXY) | 82.49 | 0.010 | 0.01% |

| 10 Year Govt Bond Yield | 2.35% | 0.01% | |

| Current Coupon Ginnie Mae TBA | 106.5 | -0.1 | |

| Current Coupon Fannie Mae TBA | 105.9 | 0.0 | |

| BankRate 30 Year Fixed Rate Mortgage | 4.06 |

Markets are flat this morning on no real news. Bonds and MBS are flat as well.

I don't think bonds are closing early today, but for all intents and purposes they are as most of the Street will be gone by noon ahead of the 3 day weekend.

The ISM Milwaukee index fell to 59.6, however the Chicago Purchasing Managers Index rose to 64 and the University of Michigan Consumer Sentiment Survey rose to 82.5.

Ready to pop the champagne over the good consumer sentiment numbers? Well, it has yet to flow through to actual spending. Personal Spending fell .1% in July, however the reason was falling energy prices. Ex-food and energy, spending increased .1%. That said it isn't that strong of a number. Personal Income rose .2%.

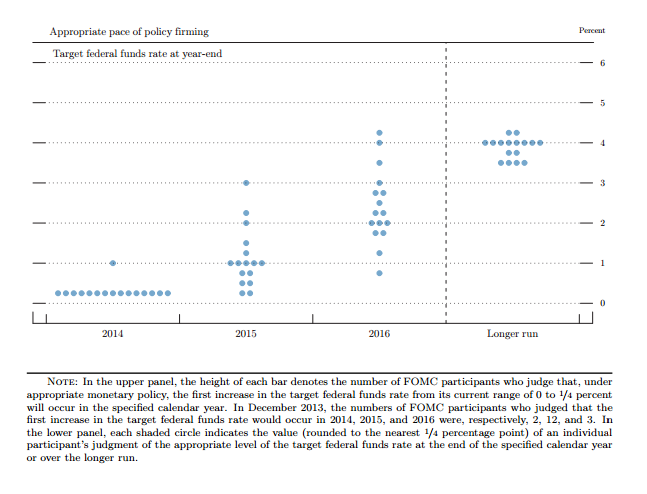

One of the interesting features of this recovery has been the disconnect between the reported unemployment rate and the actual health of the labor market. While unemployment keeps falling, the labor market still doesn't feel much better. The Fed is now looking at an index comprised of 24 indicators called the Labor Market Conditions Index (LMCI) to describe the health of the labor market. There are two pieces to the index - the current level of activity and momentum. The momentum indicator gives you clues as to where the market is going in the future. Here is what it looks like at the moment - about a year away from normalcy.

Short missive as there is not much going on. Have a happy Labor Day everyone.